A commonly encountered fork in the career road for many successful engineers is to a) continue engineering or b) manage others who engineer. To continue engineering is an obvious choice, and an often desired one.

The second path, to manage others, is also desirable but less demanded in the market place as inherently there are fewer engineering managers than there are engineers. And while moving from engineer to engineering manager also sounds like an obvious choice, it is also a stumbling block for many professionals. The skills required to be a competent engineering manager extend far beyond those required to be a competent engineer. These skills include team-building, coaching, project management, communication and others. But the skills required for engineering management that seem least akin to the engineering profession is business finance.

In addition to evaluating the technical merits of various projects, engineering managers must also evaluate the financial merits technically-sound projects competing for the same budget dollars. Large projects such as new equipment installations, building expansions, and product launches are referred to as capital projects. And the process of evaluating the financial value capital projects add to an organization is sometimes referred to as capital justification, or more commonly, return on investment analysis (ROIA).

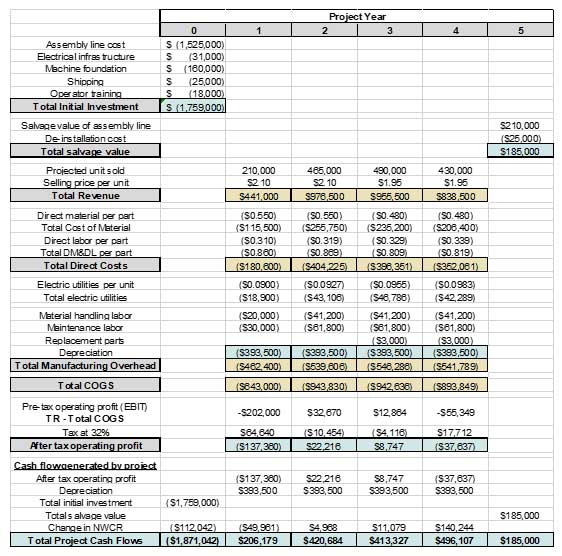

ROIA is a central component of business finance, and a “must have” for engineering managers. Far more than a “back of the napkin” guesstimate, ROIA begins by building a dynamic model containing best estimates of the initial investments, ongoing expenses, revenues and salvage values over the project’s lifecycle. Each costs and revenue estimation are also tied to a particular project year. For instance, the year a project is launched is referred to as “Year 0” and includes all the initial costs of the equipment, installation, training and related startup expenses.

Each year in the ROI model is populated with these estimates and the total years in the project lifecycle are extended into the future as far as practically possible. A completed table of these estimations looks something like this where the total estimated cash flows are tallied for each year of the project lifecycle:

Once the model is built, a manager can perform a range of analyses to determine the potential impact of the project on the organization. For instance, all of the net annual cash flows can be “rolled up” into today’s dollars—a model output called the Net Present Value, or NPV for short. After all, money earned a year, two years or five years from now is worth less than the same money invested today.

An ROIA model can also be used to perform sensitivity analysis to test the robustness of the potential returns. By creating various scenarios from the same model at high and low revenue and expense levels, managers can better understand the inherent risks of the project.

Furthermore, a manager can compare and rank a range of potential projects using their NPV’s and determine which projects are most suitable to start right away, and which are better suited for a later start.

For an engineering manager to be effective, s/he must possess at least a fundamental understanding of ROIA. Without it, they’ll resort to guess work and hunches.

To learn all the essentials of ROIA needed to succeed as an engineering, quality or manufacturing manager, sign up for the online short course titled “Return on Investment Analysis for Manufacturing”. In two short hours, you will learn how to build, use and analyze Excel-based ROI models. Plus, by signing up for the class, you will also receive all the Excel templates used in the class to apply to your projects and organization. Sign up today by clicking this link.